Hot spot funds flow to thousands of stocks to evaluate stocks to diagnose the latest rating simulation transaction

Client

Registration : The annual banking festival “2017 China Banking Development Forum and the 5th Bank Comprehensive Selection Awards Ceremony†hosted by Sina Finance will be held on August 24th at the Westin Beijing Financial Street Hotel, so stay tuned . [registration entry]

First, the market review

In the first half of this month, due to the reasons for the purchase of hedging by the textile enterprises, the near-strength and the weak arbitrage, the cotton price fluctuated upwards, rising from 14805 to 15690, and the current price difference returned to a reasonable range. However, the continuous increase of more than 10 consecutive days has caused textile enterprises to worry, and some textile enterprises have joined the letter to apply for extension. On July 21, the National Development and Reform Commission, the Ministry of Finance and China Storage Cotton jointly met to discuss whether to postpone the extension. Subsequently, the notice issued by China Reserve Cotton Management Corporation pointed out that the sixth batch of outbound inspection plans was 414,000 tons, and all of them were stocked Xinjiang cotton. In the last week, the People's Bank of China authorized the China Foreign Exchange Trading Center to announce that the tariff rate for import and export goods in August was 6.7451, compared with 6.8193 in July. The August exchange rate will further lower the reserve price in August. In addition, the recent environmental protection and production restriction policy has caused the suppression of downstream printing and dyeing factories, and the textile mills have low inventory and accumulated inventory. Multiple bad news caused Zheng cotton to fall in the last week and hit a new low for the whole year.

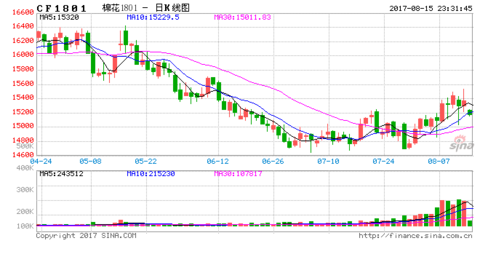

As of the night of June 28, the Zhengzhou 1709 main contract oscillated at a low level, closing at 14,695/ton, down 0.44%. Turnover of 39,814, the number of positions decreased by 4,234, a total of 148,500 hands. The original 14700 support position was converted to pressure. Large singles are 20.0% open and 12.8% more open. More than 16%, open 16.4%. As of the afternoon of June 28, the top 20 main positions were 44,182, and the number of long positions increased by 6,357, and the number of shorts was 49,087, which increased by 3517. Long and short, it is expected that the short-term Zheng cotton will consolidate between 14600-15000.

Figure 1 1709 contract day K line chart

Source: Wenhua Finance Guangzhou Futures Research Institute

Figure 2 US cotton 12 contract day K line chart

Source: Wenhua Finance Guangzhou Futures Research Institute

In terms of external disk, ICE US cotton oscillated in the 66-69 cents/lb range this month. The high yield is expected to suppress cotton prices. However, news such as high temperature and drought from time to time and better export data have also given cotton prices a certain support. August is the most critical month for determining production. It will continue to linger between production and weather, and it is estimated that it will maintain a volatile consolidation pattern.

Second, the latest news

(1) On the afternoon of July 17, Zhengshang issued an announcement on the opinions on cotton yarn futures contracts and rules and regulations. The subject of the cotton yarn futures contract is the carded 32 natural color yarn. This is a single delivery, no replacement. The basic attribute requirements are 100% cotton fiber content, 300-420 actual enthalpy coefficient, 6%-9% moisture regain, and 9 specific quality indicators, mainly composed of international indicators and Uster indicators. The beginning is mainly the delivery of the factory, and may be open to the warehouse in the later stage. The benchmark for delivery is in Henan, Shandong, and Jiangsu, and the auxiliary delivery location is Zhejiang. Import yarn delivery is prohibited at the beginning of the contract. The contract is expected to be available on August 18.

(2) The 18th China Textile and Apparel Trade Fair (New York) hosted by the China National Textile and Trade Association and the China International Trade Promotion Council Textile Industry Branch and the Frankfurt Exhibition (USA) Company on July 17th. The TEXWORLD Apparel Fabric Show in New York, ApparelSourcingUSA and HomeTextilesSourcing in New York City opened in Javits, New York. At the meeting, Chinese textile and garment enterprises actively explored the US market.

(3) According to Ruijia International News, severe flooding occurred in areas such as northern Gujarat in India, and autumn crops are expected to be damaged by about 25%. The damage caused by the flood may make the final harvest equal to last year. Indian cotton is still in the planting stage.

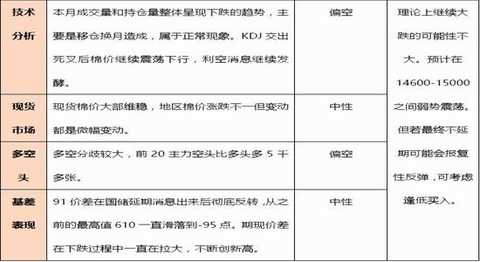

Third, operational analysis

Fourth, the current / futures market

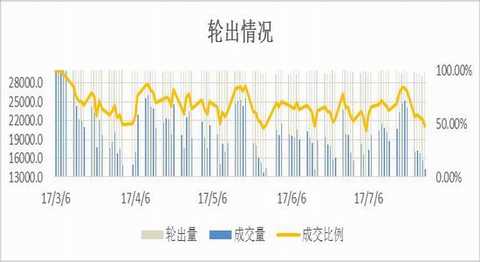

Figure 3 rounds

Source: Cotton Information Network Guangzhou Futures Research Institute

Figure 4 round 3128 and average price trend

Source: Cotton Information Network Guangzhou Futures Research Institute

The turnover rate of this month was spurred by a wave of small peaks. Due to the news of the delay, the transaction rate was suppressed to the bottom in the last week. On July 28, the turnover rate was only 47.69%, which was the third lowest turnover rate this year. The textile enterprises expecting the sixth batch of Xinjiang cotton to be released from the warehouse will have little interest in the real estate cotton auctioned before August. In addition, the rise in the exchange rate is also an important reason for the downturn. The tariff rate for import and export goods in August was 6.7451, which was 6.8193 in July, an increase of 1.08%. According to the calculation formula of reserve cotton reserve price, under the premise of unchanged foreign cotton index, the reserve price in the second week of August will be reduced by about 0.5%. If calculated according to 14,500 yuan, it will be reduced by 72.5 yuan.

Whether the average transaction price or the transaction price of 3128B grades of the reserve cotton is all the way down, under the premise of the extension of the rotation, the textile enterprises choose a large number and will only choose the appropriate cotton shot.

In the previous year, the reserve cotton price and Zheng cotton price remained highly consistent, with a correlation of 97%; the recent contract with the spot listing also reached 95%; and the correlation with the spot China cotton price index was 89%. However, the current price of the current year has deviated. The correlation between the round of cotton and the spot is 67%, only 52% with Zheng cotton, and 26% with the spot. Among them, the price of cotton inside and outside the national reserve cotton has better adjusted the price difference between domestic and foreign cotton.

Figure 5 Xinjiang cotton spot price trend

Source: Cotton Information Network Guangzhou Futures Research Institute

The price of cotton in Xinjiang is still firm this month, as spot stocks are not much, and it is expected that there will be a cotton gap of 10-15 million tons in Xinjiang in the future. However, the gap has been perfectly compensated by the 41,000 tons of Xinjiang cotton that has been released from the sixth batch. There is no room for speculation in the structural and regional problems of cotton. If the extension is finalized, the price of cotton before the listing of Xinhua will be in an oversupply state.

Figure 6 Cotton Price Index

Source: Wind Guangzhou Futures Institute

Figure 7: US cotton futures price trend

Source: Wind Guangzhou Futures Institute

Figure 8 Warehouse order quantity and effective forecast

Source: Wind Guangzhou Futures Institute

Affected by bad news, the price gap between domestic and foreign cotton continued to shrink, and it was close to Pingshui.

Zheng cotton warehouse receipts began to flow out after more than 5,000 in May. In early June, the outflow rate accelerated, reaching an average of 100-150 sheets per day. However, due to the competition from the national reserve cotton, the outflow rate slowed down again, returning to the previous average of 30-50 sheets and continuing until the end of July. As of July 28, the warehouse order plus effective forecast totaled 2,266, or 18,128 contracts. Since the warehouse receipt expires after September, the outflow pressure is high.

Fourth, basis analysis

Figure 9 Intertemporal spread

Source: Wind Guangzhou Futures Institute

Figure 10

Source: Wind Guangzhou Futures Institute

The 91 contract spread has continued to rise this year, coming out of a very beautiful trend line. However, this trend is completely reversed after the postponement news, and the spread may show a random fluctuation in the short term. Since the delayed dumping is equivalent to shifting the inventory of next year to this year, the near-strong and weak pattern of raw materials is reversed, but the essence of the impact should be 1805 contracts. The 01 contract is far less volatile than the 09 contract when the new cotton price has not been confirmed and there are many variables in the price. The short-term trend of the spread between contracts is unclear, and it is recommended to hold a position.

Fifth, the downstream situation

Figure 11 yarn price index

Source: Wind Guangzhou Futures Institute

In July, textile companies started the off-season of seasonal effects, and the restrictions on environmental protection and production restrictions for downstream printing and dyeing factories were very light in July. The cotton yarn market is lower due to lower cotton prices. Although the air spinning is also light, the price of the textile enterprises remains stable due to the low level of textile enterprises. The price of conventional yarns has dropped to varying degrees, with a drop of around 100-200/ton. The performance of the medium and high count yarns is still acceptable, and the textile enterprises are relatively smooth compared to other varieties, and the price changes are not large. Due to the low season and high temperature this month, the phenomenon of holiday or shifting of textile enterprises is still increasing. Most textile enterprises are less willing to replenish cotton, and they will buy more with them.

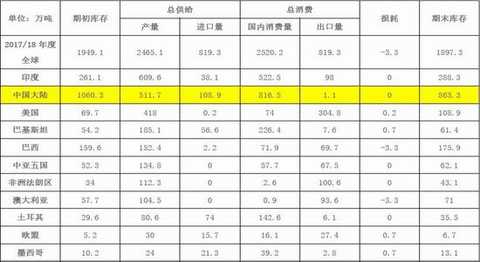

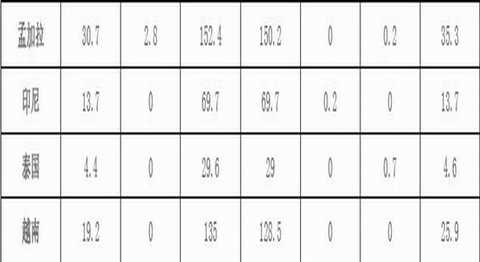

6. USDA supply and demand balance sheet

Seven, the future outlook

At the end of the month, multiple negatives were released, and the contract in recent months was strongly suppressed. Upstream supply Due to the one-month extension of the national reserve cotton supply is much larger than originally expected, the inventory of textile enterprises and the auction of the national reserve cotton can fully support the listing of new flowers, and the oversupply is very obvious. The mid-stream capital and technical forms have all suppressed the price of Zheng cotton. The downstream is in the off-season, and environmental protection and production limits are worse. The 09 contract plunged completely to retreat from the previous half-monthly increase and set a new low for the year. However, the bad news has basically been concentrated in the outbreak, and it is unlikely that it will fall sharply again in the later period. The late-month contract may be bad news for the spot price to fall. Lido news may return to the present, textile companies to replenish or postpone cancellation.

August will enter the most critical month to determine production, and the main contract will be transferred to the 1801 contract one month before the 09 contract is due for delivery. The impact of the month is the impact of weather on production. Regarding the listing price of new flowers, opinions differed. Due to the 16-year high purchase, traders lost some of their losses without hedging. This year traders should be more cautious in purchasing. According to the high yield, the purchase price should be slightly reduced.

In the short term, cotton may still show a weak range of shocks. Since August is also a traditional textile off-season, and then a lot of bad news is superimposed. In August, Zheng cotton prices are now returning to demand but want to reproduce in mid-July. The rise is probably harder. At the current price, warehouse cotton has some quality advantages compared with national cotton and stock, so cotton prices also have certain support. The kinetic energy of large fluctuations up and down is insufficient. It is unlikely that hot money will be attracted to the market. The 1801 contract is about to become the main contract, and it is necessary to pay close attention to the weather conditions and production expectations.

Guangzhou Futures

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.Enter [Sina Finance and Economics Unit] Discussion

Custom 5 Panels Trucker Baseball Cap

Do you like 5 panels trucker Baseball Cap? What is the difference between a 5-panel and a 6 panel baseball cap?

[5 Panels Trucker Baseball Cap"

A dad hat is a 5-panel (usually) baseball cap that has a slightly curved brim (pre-curved by the manufacturer), whereas a snapback is a 6-panel baseball cap with a flat brim. Both are meant to be one-size-fits-all that come with an adjustment strap in the back.

Custom 5 Panels Trucker Baseball Cap,Ladies Baseball Cap,Ball Caps For Women,Yellow Baseball Cap

Guangzhou Ace Headwear Manufacturing Co., Ltd. , https://www.custom-cap-hat.com