44% of Americans can't get $400! Don't laugh, actually we are more and more like them

Money is not saved, it is earned.

This sentence is often from the mouths of successful people around us. Compared with the older generation who are diligent and thrifty, many young people are indeed more convinced that only by continuously raising their income can they accumulate wealth, and it is difficult to save money by saving money.

But imagine, if you suddenly lost your job or naked, how long can your deposit last? If the family or yourself suddenly got a serious illness, how much medical expenses can you pay?

On May 19th, the Federal Reserve released the "Report on the Economic Well-Being of US. Households in 2016". According to the survey report, 44% of adults in the United States can't even get a contingency payment of 400 US dollars (about 2,700 yuan). In the face of unexpected situations, they have to sell items or borrow money from friends.

In a country with such a high per capita income, why are so many people unable to save money? Understanding the causes of the embarrassing situation of Americans also helps us avoid similar traps.

44% of Americans can't get $400

Since 2013, the Fed has published the "America's Household Economy Report" every year, and family emergency deposits have always been an important part of the report. In 2016, the proportion of adults with emergency deposits below $400 reached 44%, but in 2013, this proportion was as high as 50%. Although this situation has changed in recent years, it is still an unstable factor in American society.

â–² Federal Reserve "2016 US Household Economic Status Report"

â–² Federal Reserve "2016 US Household Economic Status Report"

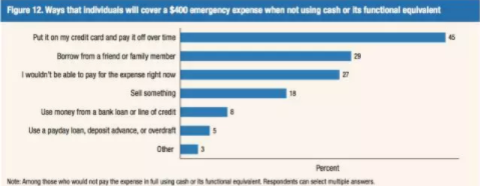

In the Fed's 2016 report, respondents were asked if they could immediately pay $400 if an accident occurred (suddenly the car broke down and needed repairs, household appliances needed to be replaced, or sudden illnesses required to pay for medical expenses). Only 56% said they could come up with the appropriate cash, or they could pay with a credit card, and they could pay off the money on the next repayment date.

Among the other 44% of respondents, 45% said they would pay by credit card, but they will overdue; 27% said they can't get the $400; and 15% said they can get friends and relatives. Borrow money there.

â–²What can I do if I can't get a $400 emergency fund? (Source: Federal Reserve's 2016 US Household Economics Report)

â–²What can I do if I can't get a $400 emergency fund? (Source: Federal Reserve's 2016 US Household Economics Report)

In addition, for the 56% of adults who can take out the money, what impact will this $400 have on his life? Among them, 13% said that they spent $400, and other aspects could not make ends meet.

It should be noted that the $400 contingency fund in the Fed's report is included in the deposit, but not exactly. Sometimes, even if you have a $500 deposit, if you suddenly get a $400 emergency, then the subsequent life will be seriously affected. So how many Americans have deposits?

According to statistics from the bank interest rate advisory firm GOBankingRates, in 2016, 69% of American bank accounts had deposits below $1,000, compared with 62% in 2015. Surprisingly, 34% of Americans say they don’t have a penny in their bank card.

â–² American bank deposits (Source: GOBankingRates)

â–² American bank deposits (Source: GOBankingRates)

Where are the Americans’ money?

As the world's largest country, Americans' income is not low, but why nearly half of Americans can't even get $400. Why do one-third of Americans have no money for deposits, and where are their money? What? This is evident from a 2013 statistic from the US Bureau of Labor Statistics.

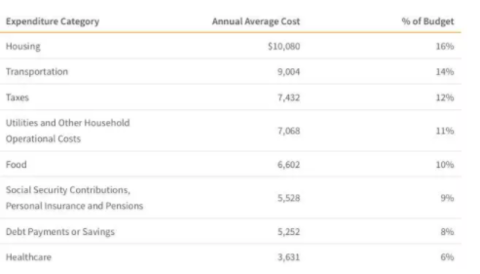

In 2013, the average income of American households was 637.84 million US dollars (about 430,000 yuan). If it is in most cities in China, it is definitely a middle-income income family.

In terms of expenses, American households have an average of 5,252 US dollars to repay debts or deposits, accounting for only 8% of annual income; taxation is 7,432 US dollars, accounting for 12%, and the remaining 51,100 US dollars are spent. Among them, the biggest expense is housing, buying a house (returning mortgages) or renting a house cost of $10080, and the related cost of utilities such as utilities is $7,068, which accounts for 33.5% of total consumption.

So, in the United States, is it cost-effective to buy a house or rent a house? According to data from the US Bureau of Labor Statistics, home buyers spend $9,552 on all aspects of housing and $7,477 on rental housing. The two seem similar. However, each small series (micro-signal: nbdnews) found from another set of data that there is a striking link between American homeownership rate and personal disposable income deposit rate.

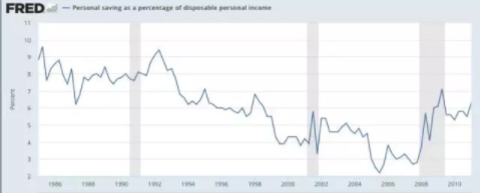

Generally speaking, when the US economy develops and personal income grows, deposits will increase because deposits are easier. However, in the 1990s, American incomes grew rapidly, but the deposit rate fell by more than 5 percentage points, the largest in the second half of the 20th century. It was in the 1990s that mortgage loans began to flourish.

â–² 1985-2010 American disposable income deposit rate trend (Source: St. Louis Fed)

â–² 1985-2010 American disposable income deposit rate trend (Source: St. Louis Fed)

The family home ownership rate in the United States has grown since the 1990s and reached its peak around 2005.

â–² 1985-2010 US housing ownership rate trend (Source: St. Louis Fed)

â–² 1985-2010 US housing ownership rate trend (Source: St. Louis Fed)

The US Atlantic Monthly explained that since the 1990s, a large number of Americans have started to buy loans, and many people have abandoned the deposit habits they developed during the economic downturn of the 1970s. By 1998, except for the richest 10% of the population, the deposit rate of the rest of the population had become negative, which was the result of the rise in mortgages.

Can Chinese people who love to climb and love to buy a house save money?

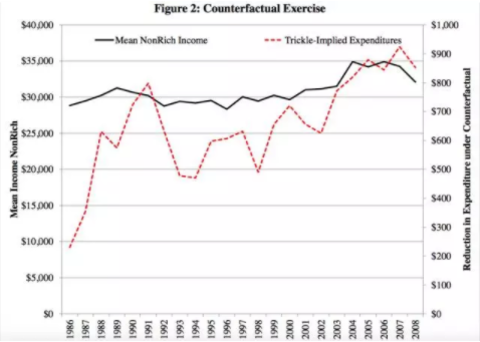

In addition to the loan to buy a house, conspicuous consumption has also led to a decline in American deposit rates. In 2012, two economists at the University of Chicago's Booth School of Business, Marianne Bertrand and Adair Morse, found that in the past 30 years, the income of ordinary Americans has grown slowly, while the income of wealthy people has increased rapidly, but at the same time, the average US deposit rate has also increased. On the decline. In this regard, the results of two professional studies show that in the past 30 years, at least a quarter of the decline in deposit rates was due to “infiltration consumptionâ€. This kind of "infiltration consumption" is actually a kind of comparison consumption. When people see other people eating food, holding luxury bags, and living a luxurious life, they will not hesitate to buy a loan even if they have no money. Studies have shown that in some wealthy states in the United States, the expenses of middle-class families have shifted from the necessities of water, electricity and food to the consumption of jewelry, furniture, gym courses and so on.

â–² Black: Non-rich household annual income; Red: Non-rich households compare consumption (Source: Marianne Bertrand and Adair Morse papers)

â–² Black: Non-rich household annual income; Red: Non-rich households compare consumption (Source: Marianne Bertrand and Adair Morse papers)

In the current era of mobile Internet, the "millennials" of the United States are facing more pressure from excessive consumption. According to statistics from GOBankingRates, 52% of young people said that the consumption brought by comparison with friends put pressure on themselves. Another 46% of young people said that the photos on the social media show their pressure.

In fact, love to climb is a common problem for young people around the world, and China is no exception. Many young people are pursuing luxury bags, the latest digital products, and traveling abroad when their income is not high enough. And now the credit card payment on the bank credit card and mobile phone side also facilitates this advanced face consumption. Not only that, this kind of consumption is also very popular in universities, so there is a "naked loan."

Before, people said that Chinese people love to save money and do not like consumption. The savings rate has been at the forefront of the world, reaching about 50%. But in fact, a large part of the high savings rate of Chinese nationals is caused by high savings from the government and enterprises. Data from the International Clearing House show that between 2000 and 2008, 80% of China's total national savings grew from the government and corporate sectors, not from households.

In addition to the comparison and face consumption, Chinese young people still love to buy a house. According to a report by HSBC in April, the housing ownership rate of China's “millennials†(ie, after 80s and 90s) reached 70%, while 40% of young people bought houses by their parents. There are more and more young people buying houses, but most of them have to rely on their parents' deposits to provide a down payment, and they have to pay the loan every month. This will inevitably reduce the deposits of the older generation and increase the difficulty of deposits for young people.

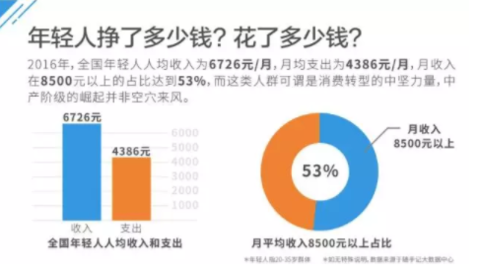

However, the good news is that there is a set of data showing that the stereotypes of young people who love to compare, love consumption, and not deposit are gradually being broken. According to the "2017 Young People's Consumption Trend Data Analysis" jointly published by many companies, in 2016, the per capita income of young people in the country was 6,726 yuan/month, the monthly average expenditure was 4,386 yuan, and the monthly deposit reached 2,340 yuan.

â–²Image source: "2017 young people consumption trend data analysis"

â–²Image source: "2017 young people consumption trend data analysis"

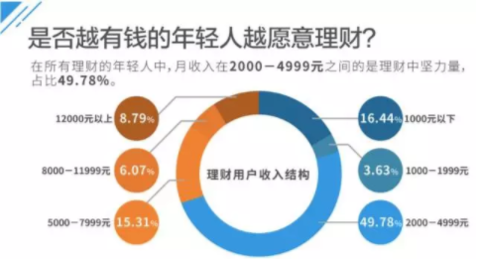

Moreover, the younger the income, the more financially conscious. It can be seen that compared with Americans, the Chinese people's habit of saving money is still very strong.

â–²Image source: "2017 young people consumption trend data analysis"

â–²Image source: "2017 young people consumption trend data analysis"

Enter [Sina Finance and Economics Unit] Discussion

New Sexy Bra,Mesh Women's Underwear,Transparent Mesh Women's Underwear

Shaoxing hjh clothes.co.ltd , https://www.hjhclothes.com